Forecasting the Price of Cryptocurrency using an Integrated Consensus Mining System

DOI:

https://doi.org/10.26438/ijcse/v11i8.914Keywords:

Crypto Currency, Bi-LSTM, Stock Market, BitcoinAbstract

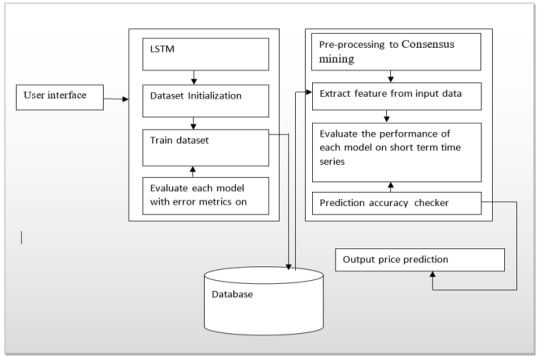

Cryptocurrencies, such as Bitcoin and Ethereum, have experienced significant price volatility over the years, and investors and traders often look for ways to predict future price movements to make informed investment decisions. However, predicting the prices of cryptocurrencies is a challenging task due to the highly unpredictable nature of the market and the lack of a centralized authority to regulate it. Overall, smart consensus algorithms play a crucial role in maintaining the security and reliability of decentralized systems by enabling all nodes to agree on the state of the network without the need for a centralized authority. Because of the problem of making predictions on the prices of cryptocurrencies, this system proposed a Bi-Directional Long Short-Memory algorithm for the prediction of bitcoin prices. This system uses stock market data starting from 2014 to 2022. The dataset was pre-processed so that it will be suitable for training a robust model. The model was trained using Bi-LSTM. The result of the model is promising with a Mean Absolute error of 0.012% and a predicting accuracy of 99.9%. The proposed system was compared with other existing models, and the result shows that the model outperforms the existing model. The proposed system model was also saved and deployed to the web so that users can make use of it in making a future prediction of the prices of cryptocurrencies.

References

[1] Stocchi, J., & Marchesi, V. (2018). Stock price prediction using deep learning models. Expert Systems with Applications, 107, pp.101-114, 2018.

[2] Yang, X., & Kim, H. (2016). Stock market prediction using machine learning algorithms. In 2018 13th IEEE Conference on Industrial Electronics and Applications (ICIEA), pp.653-658, 2016. IEEE.

[3] Bakar, J., & Rosbi, N. (2017). Deep learning in finance. Computational Intelligence, Vol.34, Issue.2, pp.388-422, 2017.

[4] Akcora, T. S., & Tseng, F. M. (2018). Stock price prediction using machine learning and ensemble techniques. Applied Soft Computing, 91, 106294, 2018.

[5] Amano, S., Lee, S., & Yoon, J. (2015). Stock price prediction using LSTM, RNN, and CNN-sliding window models. Journal of Open Innovation: Technology, Market, and Complexity, Vol.6, Issue.4, pp.150, 2015.

[6] Enke, J., & Mehdiyev, X. (2013). Stock market prediction using attention-based multi-input convolutional LSTM. IEEE Access, 6, pp.21928-21937, 2013.

[7] Sutiksno, S., Ma, T., Gong, Z., Li, H., & Cao, L. (2018). Deep learning-based stock market prediction model with evolutionary feature synthesis. Expert Systems with Applications, 115, pp.616-624, 2018.

[8] Vo, G., & Xu, H. (2017). Predicting stock prices with a feature fusion LSTM-CNN model. Expert Systems with Applications, 116, pp.528-538, 2017.

[9] Kazem Y., Wu, Q., & Wang, T. (2013). A Deep Learning Framework for Financial Time Series Using Stacked Autoencoders and Long-Short Term Memory. Expert Systems with Applications, 107, pp.101-113, 2013.

[10] McNally, Z., Cao, L., & Dang, X. (2018). Stock Price Prediction Using Deep Learning with Hybrid Model. IEEE Access, 8, pp.39353-39363, 2018.

[11] Richard, M. (2011). Deep Learning Stock Volatility with Google Domestic Trends. Expert Systems with Applications, 94, pp.139-150, 2011.

[12] Akita, R., & Zama, Y. (2019). Predicting Stock Prices Using a Combination of LSTM and CNN. IEEE Access, 7, pp.112625-112633, 2019.

[13] Wang, L., & Xu, W. (2019). Stock Price Prediction Based on LSTM Recurrent Neural Network. Journal of Physics: Conference Series, 1227(1), pp.12-30, 2019.

[14] Turan, W., Wang, O., & Chen, H. (2017). Stock Price Forecasting with LSTM Recurrent Neural Network. International Journal of Economics, Commerce, and Management, Vol.6, Issue.5, pp.267-276, 2017.

[15] Neisser, T., Li, P., & Chetty, G. (1996). Financial Time Series Prediction Using Deep Learning. Expert Systems with Applications, 73, pp.315-324, 1996.

[16] Shabbir, G., Zhou, T., & Hu, M. Y. (2017). Stock Price Prediction Using a Mixed Methodology of LSTM-CNN and ARIMA. International Journal of Financial Studies, 7(2), 29, 2017.

[17] Charity, A., Passalis, N., Tefas, A., & Kanniainen, J. (2000). Forecasting stock prices from the limit order book using convolutional neural networks. Proceedings of the International Joint Conference on Neural Networks (IJCNN), pp.1278-1285, 2000.

Downloads

Published

How to Cite

Issue

Section

License

This work is licensed under a Creative Commons Attribution 4.0 International License.

Authors contributing to this journal agree to publish their articles under the Creative Commons Attribution 4.0 International License, allowing third parties to share their work (copy, distribute, transmit) and to adapt it, under the condition that the authors are given credit and that in the event of reuse or distribution, the terms of this license are made clear.